Facebook

Facebook Google

Google GitHub

GitHub Linkedin

LinkedinVPPs Are Growing, but Not Fast Enough for Demand

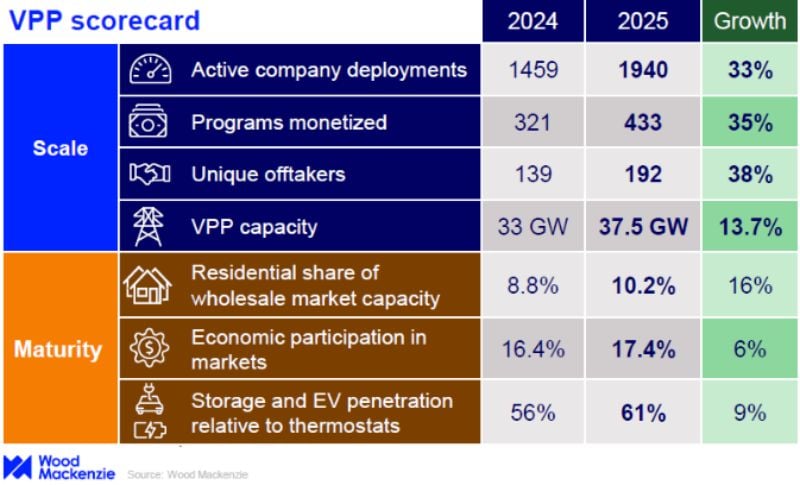

VPP deployments jumped 33% in 2024, but new capacity remains muted.

The virtual power plant (VPP) sector grew 33% last year, reaching 1,940 deployments across more than 430 programs, according to a Wood Mackenzie report. Offtakers expanded to 192, with over two dozen now sourcing 100 MW or more apiece.

Despite strong market activity, overall VPP capacity growth is lagging far behind deployments, rising just 13.7% to 37.5 GW. Program caps, accreditation changes, and other market barriers slowed expansion.

Wood Mackenzie noted that residential uptake remains limited. The share of wholesale market capacity from residential consumers grew by 16% in 2024—reaching double-digits for the first time, from 8.8% to 10.2%.

Power lines at sunset. Image used courtesy of Pexels

Technology Trends

A VPP aggregates distributed energy resources (DERs), such as batteries, electric vehicles, or smart devices, to be dispatched as a single power plant-like resource for grid services. While utilities set the rules and funding, it’s mostly aggregators and software providers that operate these customer-owned assets day to day. In North America, VPP deployments—including EVs or batteries—are now 61% as common as those with smart thermostats, up from 56% in 2024.

In the last few years, VPPs have launched across North America and globally with growing support. Tesla's VPP enrollment topped 100,000 Powerwalls last year. The company reported that dozens of its VPPs worldwide helped balance supply and demand in 2024's summer heatwave, including over 125 MW delivered to California's grid during peak demand.

Wood Mackenzie reported that only 17.4% of VPP capacity is tied to energy markets. Most is in emergency capacity, indicating that VPPs' role in grid-balancing remains limited.

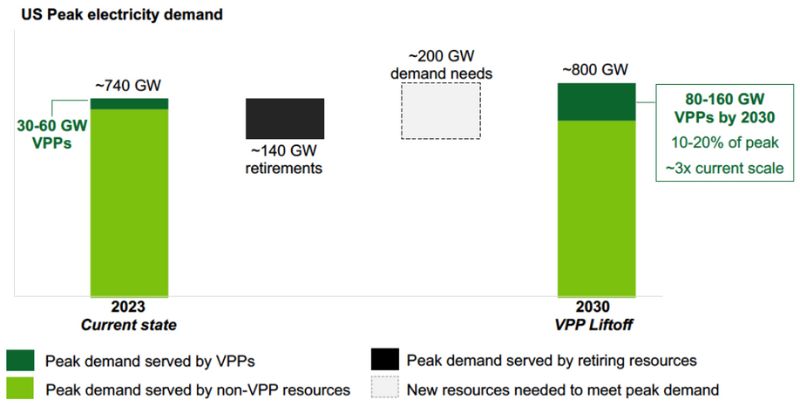

A 2023 analysis by the U.S. Department of Energy suggests that tripling current VPP capacity to 80-160 GW by 2030 could handle up to 20% of peak load and save more than $10 billion annually by eliminating the need to build new generation, transmission, and distribution capacity.

Estimates of VPPs' value in the U.S. electricity system by 2030. Image used courtesy of the DOE

A major technical bottleneck is data access, with inconsistent standards between federal and state regulations on advanced metering infrastructure (AMI). This misalignment has limited residential and small commercial participation in wholesale markets. On the technology side, some DER OEMs are prioritizing customer-centric control in ways that reduce performance and utility confidence.

Another emerging focus is coordination across different DER types. Utilities and operators are pressing for better edge DERMS capabilities that can dynamically group assets and manage batteries, EVs, and thermostats in real time. Many current aggregations still function in silos, which limits flexibility and response speed. Proving cross-technology optimization is critical if VPPs are to provide daily balancing rather than remaining concentrated in emergency demand response.

Regional Growth and Utility Programs

California, Texas, Massachusetts, and New York dominated VPP expansion, accounting for 37% of all deployments.

California remains a top market, but providers have warned that growth could stall without new funding for the state’s Demand Side Grid Support (DSGS) program, which is especially critical for behind-the-meter storage. The battery program launched in 2023 and has grown to over 720 MW of enrolled capacity, according to the California Solar and Storage Association.

PJM (Pennsylvania-New Jersey-Maryland Interconnection) and the Electric Reliability Council of Texas are now among the largest VPP hubs, thanks to heavy commitments from utilities serving data centers. The two systems now account for the greatest disclosed VPP offtake capacity.

Meanwhile, utility tariffs and market design gaps still limit the Southwest Power Pool and the Midcontinent ISO.

VPP scorecard. Image used courtesy of Wood Mackenzie

Looking ahead, the question of who controls the VPP asset base remains unresolved. Hardware vendors tend to support utility ownership of DERs under the Distributed Capacity Procurement model, while aggregators and software providers argue this approach will crowd out private capital and limit competition.