Facebook

Facebook Google

Google GitHub

GitHub Linkedin

LinkedinFuture-Proofing Energy Security: The Case for Regional Battery Supply Chains

Reimagining the production of cathode active materials (CAM) can help make regional battery manufacturing both technically feasible and financially compelling.

The energy transition isn’t just about decarbonization—it’s about security, scalability, and sovereignty.

As demand for electricity skyrockets—driven by the electrification of everything from transportation to AI-fueled data centers—batteries have become a cornerstone of modern infrastructure. Yet while demand for storage explodes, the supply chains behind it remain fragile, geographically concentrated, and exposed to market and geopolitical shocks. If we want a resilient clean‑energy economy, we must rethink where and how batteries are built.

Today, nearly 80% of the world’s lithium is coming from just three countries: Chile, Argentina, and Australia. And China dominates when it comes to processing, producing over 60% of global lithium and about 75% of the world’s battery cells and components. This level of concentration poses an enormous risk. It affects the pace of innovation and economic and national security. Russia’s invasion of Ukraine further exposed reliance on nickel from conflict‑adjacent regions.

Lithium fields in the Atacama desert of Chile, one of the three leading nations for lithium production. Image used courtesy of Adobe

Supply insecurity is not hypothetical. It is a daily operational risk that bleeds into commodity markets, corporate balance sheets, and household electricity bills. That risk is no longer theoretical, and it’s immediate and escalating.

The U.S. government recently announced sweeping new tariffs as part of the so-called “Liberation Day” global trade policy. These measures will raise total duties on Chinese-made batteries and battery energy storage systems (BESS) imported into the U.S. to a staggering 155.9% by January 2026. That’s not just an economic challenge, it’s a wake-up call. The cost of battery manufacturing has already risen nearly 20% in recent years due to existing tariffs and material shortages. Now, with 155.9% duties looming, domestic production is a strategic imperative.

The message is clear: build at home. But tariffs alone will not create factories or technicians. Without technology that can compete on cost and sustainability, high import duties simply raise prices for end users and slow the adoption of clean technologies.

We Can’t Copy-Paste Our Way Out of This

Some argue we should simply replicate China’s approach—fast, high-volume, cost-driven manufacturing. But that strategy won’t work. Not politically. Not economically. And certainly not environmentally.

Efficient, localized EV battery production is critical to energy security. Image used courtesy of Adobe

China has invested over $231 billion in subsidizing its EV and battery industries. This is nearly six times what the U.S. has invested to date. It has spent decades optimizing its supply chains, often in ways that don’t align with Western environmental or labor standards. Setting up a lithium iron phosphate (LFP) plant in China currently costs about 75% of what it would in the U.S. or Europe using today’s methods. The gap is even wider for nickel-based chemistries, due to high environmental compliance costs.

So, no—copying China’s model isn’t just impractical—it’s unnecessary. We don’t need to outspend or out-subsidize. We need to out-innovate.

Innovation That Enables Localization

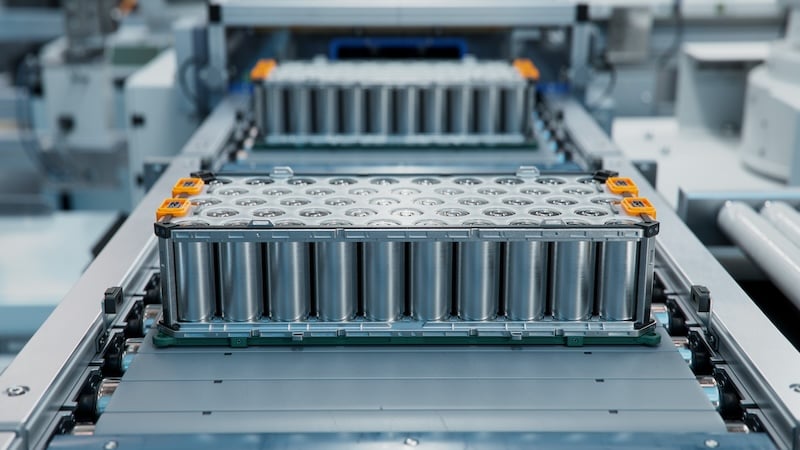

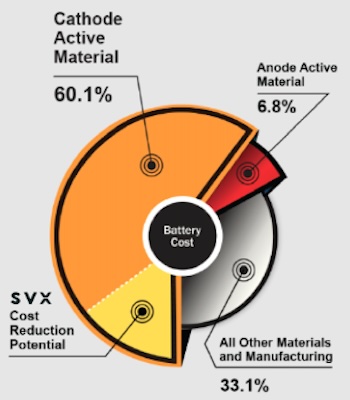

At Sylvatex, we’re not just onshoring battery materials—we’re redefining how they’re made. We are reimagining the production of cathode active materials (CAM). These are the most expensive and energy-intensive part of a battery, cathode active materials (CAM).

The cathode active material (CAM) is the most expensive part of a battery. Image used courtesy of Sylvatex

Our waterless cathode manufacturing platform directly addresses the three most critical barriers to domestic production:

- Cost

- Scalability

- Environmental impact.

By eliminating water from the production process—a resource typically required in vast quantities—we’re not only reducing waste but also unlocking significant capital and operational savings. Our streamlined, high-efficiency approach cuts down on energy usage, broadens available material inputs, and removes costly post-processing steps. These aren’t incremental improvements. They’re paradigm shifts that reduce the total cost of ownership and emissions footprint from day one.

With our technology, we’ve demonstrated that it’s possible to produce CAM using less infrastructure, at a lower cost, and a fraction of the environmental footprint. We’re making regional manufacturing both technically feasible and financially compelling. Now, we’re focused on scaling in the U.S. and in other regions that see battery production as a pillar of economic and energy security.

Building With What We Already Have

The United States already possesses the assets to scale: rail‑connected brownfield sites, abundant renewable power, and world‑class universities.. Add to that a skilled and diverse workforce hungry for next-gen manufacturing jobs, and we have a real opportunity.

What we need now is alignment: alignment between public and private sectors, between federal and local governments, between climate goals and industrial policy.

Federal programs such as the Inflation Reduction Act (IRA), the Department of Energy’s Loan Programs Office, and the CHIPS and Science Act are beginning to close financing gaps for first‑of‑a‑kind facilities. The IRA in the U.S. and the EU’s Net Zero Industry Act are major steps in the right direction. These policies are creating tailwinds for localized supply chains by incentivizing domestic content, clean manufacturing, and innovation. But incentives alone aren’t enough.

We need public-private partnerships that fast-track permitting, ease regulatory bottlenecks, support workforce development, and prioritize first-of-a-kind commercial-scale deployments of next-gen technology.

We also need clear, consistent signals from policymakers. Tariffs are one lever, but we must follow through with long-term investment in American innovation and infrastructure.

Additionally, tariffs are hindering regional collaborations with our neighbors. A North American bloc linking U.S. cathode plants, Canadian mid‑stream processors, and Mexican cell assemblers would combine resource security with continental comparative advantage while avoiding single points of failure. Similar regional compacts are already under discussion between the European Union and its near neighbors.

The Hidden Costs of Inaction

To be clear, the cost of not investing in regional supply chains is far greater than the price of tariffs or subsidies.

If the U.S. and its allies remain dependent on a single country for the majority of their battery components, we’re at constant risk of supply shocks, price manipulation, and technological stagnation. We risk falling behind in a race that touches everything from clean energy to national defense.

Nickel Manganese Cobalt Oxide (NMC) powder is an important material for the manufacture of lithium-ion batteries. Image used courtesy of Sylvatex

Delays also carry environmental costs. A study by the Rocky Mountain Institute found that every gigawatt‑hour of storage deferred past 2030 locks in roughly a quarter‑million tons of additional CO₂ from backup fossil generation. Inaction is not neutral—it is retrograde.

The transition to renewable energy is already underway. However, the next phase is about building the infrastructure backbone that will sustain it. Batteries are no longer niche; they’re foundational. And we can’t afford to build that foundation on sand.

The Opportunity Is Now

Battery production is expected to more than double by 2030. This market is projected to reach $480 billion globally. The countries that build resilient, regional supply chains by investing in innovation and sustainability will shape the next century of industrial leadership. Further, countries that pair forward‑looking policy with breakthrough manufacturing will seize outsized economic and strategic rewards. Those that hesitate will inherit outdated cost structures.

This is our moment to shape the future—intelligently, sustainably, and competitively. We don’t need to outspend or out-subsidize China. We need to out-innovate them.

Batteries have moved from the margins to the mainstream of global infrastructure. If we wish to future‑proof energy security, we must build supply chains as resilient as the clean‑energy systems they support. Let’s build smarter. Let’s build here.