Facebook

Facebook Google

Google GitHub

GitHub Linkedin

Linkedin$331.8 Billion Electric Cost Disparity Between Monopoly and Competitive States Revealed

The Retail Energy Supply Association (RESA), a trade association representing competitive retail energy suppliers, released new research on electricity price trends that exposes an overwhelming cost disparity between monopoly and competitive states. The researchers noted that the electricity industry as a whole is facing unprecedented market conditions including lower demand for electricity and a natural gas revolution resulting from fracking and the switching of coal-based electricity generation to natural gas.

Despite these market conditions, they found that consumers in states that allow retail energy competition are paying less for electricity, while consumers in monopoly states are paying more.

"The electricity industry has been struck by conditions it has never seen or experienced before," said Tracy McCormick, RESA Executive Director. "In the last decade, we have seen either flat or lower demand for electricity combined with the shift toward natural gas. But what's most unsettling is that, while it affects every single state, it is consumers in monopoly states who are paying the price."

In the white paper entitled, "The Great Divergence in Competitive and Monopoly Price Trends," Philip O'Connor, Ph.D. and Muhammad Asad Khan examined data from the U.S. Energy Information Administration (EIA) and compared the weighted average price trends of the 35 U.S. monopoly states with the 14 U.S. jurisdictions that allow competition.

Their research reveals that between 2008 and 2017, the all-sector annual weighted average price for electricity in the 35 monopoly states was 18.7% higher in 2017 than in 2008. On the other hand, the all-sector annual weighted average price for the competitive retail markets was found to be 7% lower in 2017 than in 2008. The research also found that the cost implications of such a difference are "staggering."

Analysis

The analysis, which did not include Alaska and Hawaii due to their unique geographic situations, showed that if the annual percentage price changes in the 35 monopoly states had followed with the percentage prices in competitive jurisdictions, consumers in the monopoly states would have paid almost one-third of a trillion dollars ($331.8 billion) less.

Alternately, if the same price trend patterns that occurred in the monopoly group had prevailed in the competitive jurisdictions, the cost to consumers in the 14 choice markets would have been higher by $225.6 billion.

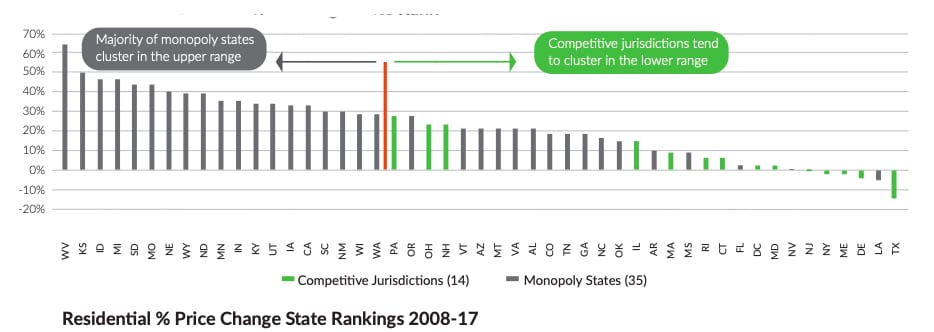

Graph of residential price change across 48 states (excluding Alaska and Hawaii) from RESA report. (See Publication) (Click image to enlarge)

Graph of residential price change across 48 states (excluding Alaska and Hawaii) from RESA report. (See Publication) (Click image to enlarge)

The research also reveals one partial explanation for this cost disparity in the way competitive markets and monopoly regulation treat power plant utilization. While plant utilization has dropped in greater proportion in monopoly states, plants in those states are given full cost recovery from the state government. Consumers have to absorb those costs. In contrast, if plants are underutilized in competitive markets, they will face adverse financial consequences, but in competitive markets, investors pay the price, not customers.

Two Parallel Regulatory Systems

In the white paper, they pointed out that for the past two decades, two different electricity regulatory regimes have existed side-by-side in the U.S.

They said in the white paper that thirty-five states in the contiguous United States mostly have adhered to the traditional, vertically-integrated monopoly model. Seven of those thirty-five states regulate rates in the conventional way while permitting only highly-restricted access to regional power markets, mainly for a portion of large customers.

Also, according to the findings, Fourteen other jurisdictions, thirteen states and the District of Columbia, allow for in-depth retail electricity competition that serves almost all customers at market prices. In these jurisdictions, utilities divested their generation assets, or regulation required a restructuring of their businesses that resulted in competitive affiliates.

These competitive retail markets account for about one-third of the nation's electricity consumption and generation, the findings indicated. With the exception of Texas, market-based electricity supply pricing and consumer choice of electricity suppliers is concentrated in the northeastern quadrant of the country.

Differences in Capacity Factor

They said that price disparity partially results from the greater decline in capacity factor (the ratio of the power generated to their total generating capacity in their power plant portfolio) in the monopoly states than in the competitive states. At the same time, they noted that this capacity factor decline is larger, both nominally and proportionally in the monopoly states compared to the competitive jurisdictions.

They report that the average capacity factor in the monopoly states declined from 52.2% in 1997 to 42% in 2016 (the most recent year for which EIA data are available). That is about a one-fifth decrease (19.5%) compared to a more modest decline in average capacity factor in the competitive markets from 49.4% in 1997 to 45.8% in 2016, a proportional drop of 7.3% or about one-fourteenth.

They point out that way the regulations in the competitive states versus those the monopoly states handle the decline in capacity factor results in consumers footing the bill in monopoly states. Whereas, investors make up the difference in competitive states.

Conclusion

"After conducting our research, we found it poses an important challenge for policy-makers," said Muhammad Asad Khan, co-author of "The Great Divergence in Competitive and Monopoly Price Trends." "That challenge is to come to a clear and accepted explanation for the price divergence so that it can then become the basis for future reform that benefits consumers in every state."

Publications

O'Connor, P., M.A. Khan, The Great Divergence in Competitive and Monopoly Electricity Price Trends. Retail Energy Supply Association, Sept. 2018.