Facebook

Facebook Google

Google GitHub

GitHub Linkedin

LinkedinThe Case for Electric Water Heaters as Storage for Demand Flexibility

A report out of Australia identifies domestic electric water heaters as a promising source of flexible demand, capable of storing energy equivalent to more than 2 million home batteries.

Smart electric water heaters could supply up to 30 gigawatt-hours (GWh) of daily flexible demand capacity in Australia’s power grid while substantially reducing residential greenhouse gas (GHG) emissions.

Air-source heat pump. Image used courtesy of Stiebel Eltron

Switching from gas water heaters to electric heat pumps or resistance heaters retrofitted with demand-response controls would yield significant household storage potential, amounting to more than 2 million home batteries.

The University of Technology Sydney (UTS)’s Institute for Sustainable Futures published a 101-page report—commissioned by the Australian Renewable Energy Agency— exploring the benefits and challenges of replacing conventional GHG-emitting gas systems with alternatives that support renewable integration. That strategy could include increasing electric heat pump uptake or retrofitting existing electric heaters with smart controls for demand flexibility. With around 50% of Australian homes already using electric water heaters—and the other half using gas systems—the infrastructure for such a transition is already well-established.

Types of Domestic Water Heaters and Their Benefits

Two types of water heaters offer notable advantages and cost considerations: air-source heat pumps and resistance heaters. The former option supplies three to five times the efficiency of the latter, which helps offset the comparatively higher installation cost since it’s cheaper to operate. On the other hand, resistance heaters are inexpensive to install but relatively costly to operate. Still, when paired with smart controls, they provide better demand flexibility to offset intermittent energy supply from renewables like rooftop solar panels, absorbing off-peak energy.

How each type of water heater stacks up regarding peak electrical loads, non-installation costs, and space requirements. Image used courtesy of the UTS Institute for Sustainable Futures (page 4)

Meanwhile, conventional instantaneous gas systems account for about 25% of all water heaters sold in Australia and are the default in homes with gas connections; they’re also cheap to produce and provide a virtually unlimited hot water supply. Other less-popular technologies include gas storage systems and solar with gas boosters, each claiming 14% and 5% of Australia’s total water heater stock, respectively.

But with more renewables being added to the grid, so arises a demand for off-peak renewable energy storage providing flexible demand response capabilities. This need is becoming more prominent as rooftop solar panels are gaining widespread adoption across Australia. And the country’s cumulative solar photovoltaic (PV) installations totaled 25.4 GW in 2021, according to the most recent available data from the International Energy Agency. Solar PV’s contribution to Australia’s electricity demand has now surpassed 15%, compared to about 5% globally.

Residential battery energy storage system (BESS) adoption is rising in Australia. As EE Power reported earlier this year, the country charted a 55% increase in BESS uptake in 2022, with over 47,000 installations totaling 589 megawatt-hours.

Electric Water Heater Opportunities

Domestic hot water usage claims one-fifth of residential GHG emissions in Australia and one-fourth of household energy use. Electric water heaters could help reverse this trend and support the government’s 2030 target to reduce carbon emissions by 43%. They provide increased efficiency and opportunities for fuel switching and can support the growing capacity of renewables connected to the power grid.

The report says potential solutions would likely involve optimizing existing electric storage systems to include output from renewables, increasing heat pump installations in suitable areas, and decreasing the installed base of gas water heaters.

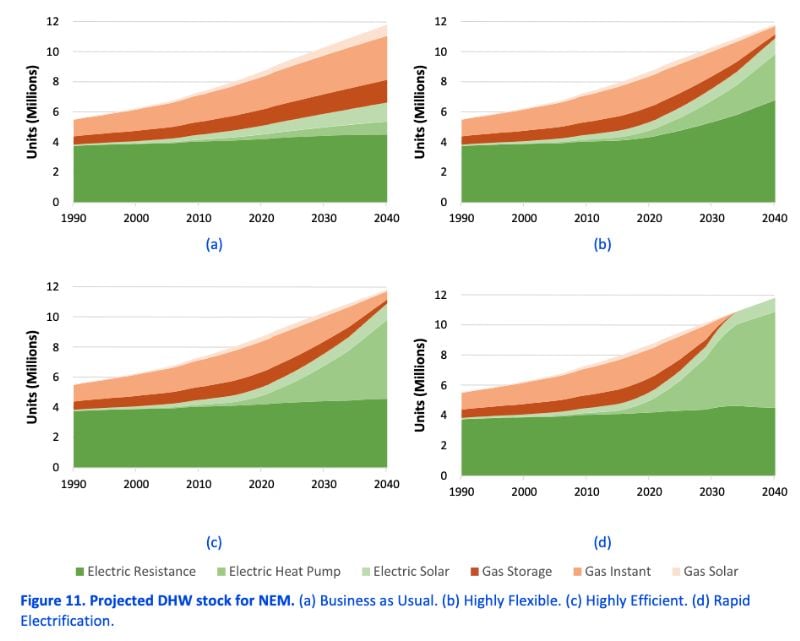

The UTS Institute for Sustainable Futures mapped out four potential scenarios, including a “business-as-usual” case and three alternatives focusing on flexibility, efficiency, or both benefits. Overall, continuing the current status quo would miss an opportunity to use domestic water heaters to store flexible demand ranging from 15 to 31 GWh daily.

This decision tree outlines ideal configurations of domestic hot water and flexible demand systems under different circumstances demanding varying efficiency and flexibility. (Note: “DRED” stands for demand response enabling device.) Image used courtesy of the UTS Institute for Sustainable Futures (page 5)

Barriers Limit Uptake

The report also found that phasing out gas water heaters would provide annual savings to consumers of $4.7 to $6.7 billion by 2040. And electrification of water heaters could cut emissions by three to five times more than the current forecasts.

Under the report’s business-as-usual case—assuming projected trends, no forced gas phase-out, and slow adoption of domestic water heaters with flexible demand to 60% by 2050—annual GHG emissions from water heating will stay at 3.5 metric tons (Mt) of carbon dioxide in 2040, of which 85% will come from gas systems.

Estimated domestic hot water stock across Australia’s National Electricity Market (NEM) through 2040 for each scenario detailed in the report, as labeled at the bottom. Image used courtesy of the UTS Institute for Sustainable Futures (page 36)

The “highly efficient” and “highly flexible” scenarios can reduce emissions by 1.2 to 1.4 Mt, with 44-39% of gas hot water systems emissions. The highly efficient course assumes a gradual phase-out of gas water heater sales by 2040, replaced by electric heat pump units, and 100% uptake of domestic water heaters with flexible demand by 2050. The highly flexible track makes a similar assumption, with gas units displaced by electric resistance units and assuming 100% uptake by 2045.

The “rapid electrification” scenario assumes no domestic gas water heating sales after 2025 and growing heat pump sales to replace gas and reach 100% uptake of domestic water heaters with flexible demand by 2035. This would slash carbon emissions even further to 0.71 Mt.

But despite these potential advantages, there are still barriers to widespread electric water heater adoption and tapping into the flexible demand capacity. While government incentives help boost these goals, the potential is hindered by higher capital costs, supply chain challenges, and existing policies emphasizing gas. For example, resistance storage water heaters paired with smart controls offer high demand flexibility with lower upfront costs and are easier to retrofit than heat pumps; still, the short-term emissions and operating costs are higher, so the value proposition in unlocking this potential flexibility is limited.